Facing the reality that you may never return to your previous work due to a serious injury or illness is deeply confronting. For many Australians, this isn’t just a medical or emotional challenge. It’s a financial one too. If you’ve found yourself in this position, you might be entitled to a total and permanent disability (TPD) payout through your superannuation fund.

What’s surprising to many is that TPD insurance is often included in superannuation accounts, even if you’ve never actively applied for it. And if you have multiple super funds, you could potentially be eligible to make multiple TPD claims. Yet despite how common TPD insurance is, most people don’t know they have it or how to access the benefits when they need them most.

This comprehensive guide to a TPD payout from a superannuation fund will walk you through everything you need to know: eligibility for a TPD super payout, how much you can expect, how long it typically takes, whether you’ll pay tax on a TPD payout if you’re under 60, and importantly, how our experienced TPD lawyers at Withstand Lawyers can support you throughout your claim.

Am I Eligible for a TPD Insurance Payout Through My Super Fund?

To check if you have Total and Permanent Disability (TPD) insurance in your superannuation fund, you can review your most recent superannuation member statement. However, TPD insurance may have been included in a previous super account or employment period, so we strongly recommend contacting our TPD lawyers to ensure you’re not overlooking a potential claim.

If you do hold TPD insurance through superannuation, whether you’re eligible to make a claim depends on the specific terms of your super fund’s policy. Each superannuation fund has its own definition of total and permanent disability, so it’s vital to examine the insurance terms of every fund you’ve contributed to.

Generally, you may be eligible to claim a TPD payout from super if:

You’ve been unable to work for an extended period (usually 3 to 6 months) due to a serious injury or illness.

You’re unlikely to return to work for which you are reasonably suited by your education, training, or experience (ETE).

👉 Read our step-by-step guide to making a TPD claim through your superannuation fund

Want to speak to someone who can help? At Withstand Lawyers, we can help determine whether you have TPD insurance in your super, assess if you meet the TPD claim eligibility criteria, and explore whether you can make multiple claims through different super funds.

Call us on 1800 952 898 for a free claim assessment with our experienced superannuation TPD lawyers.

How Much Is a Typical TPD Payout From My Super Fund?

The TPD payout amount you may receive depends on the level of TPD insurance coverage included in your superannuation fund. This amount is usually listed in your most recent superannuation member statement under insurance benefits.

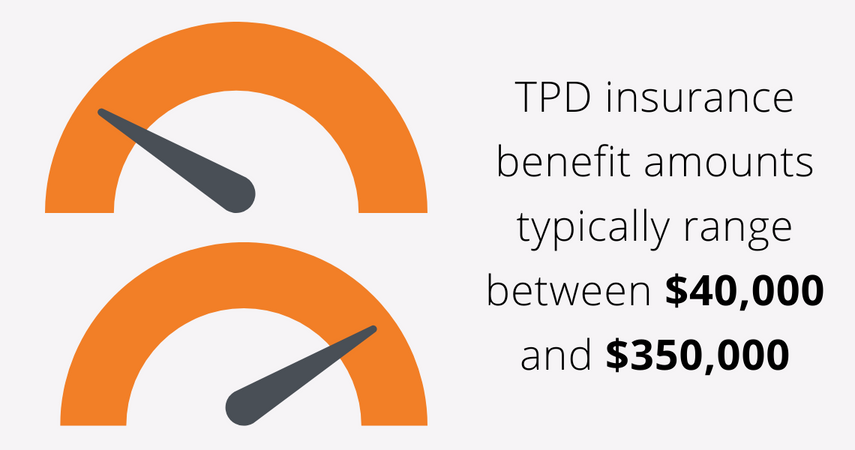

On average, typical TPD payouts from superannuation range from $70,000 to $2,000,000, depending on your policy, employment history, and contributions. Some workers may have higher or multiple TPD benefits if they hold coverage across several super funds.

If you make a successful TPD claim, you may be given the option to withdraw your balance from your employers superannuation contributions. It is important, however, to recognise that there may be financial/tax implications depending on specific factors.

Although our TPD lawyers are unable to provide you with financial advice, we can assist you in ensuring you get the right advice prior to withdrawing your TPD benefit. If you would prefer to read more about the tax and Centrelink implications you can click here.

How Long Does It Take to Get a TPD Payout from a Super Fund in Australia?

In most cases, it takes between 6 to 12 months to receive a TPD (Total and Permanent Disability) payout from your superannuation fund. However, the TPD claim process can be shorter or longer depending on your specific circumstances.

The length of time it takes to finalise a TPD insurance claim depends on:

The complexity of your claim

The amount of medical and employment documentation required

How quickly your super fund and insurer respond

Whether your claim is disputed or requires further review

Straightforward claims with clear medical evidence and eligibility can be processed more quickly, sometimes in as little as a few months. However, complex TPD claims may take longer than 6–12 months for a decision.

At Withstand Lawyers, our experienced TPD lawyers handle hundreds of TPD claims and understand what each superannuation fund and insurer requires. We work to streamline the process, reduce delays, and help you claim the maximum TPD payout available.

Contact us today for a free claim assessment. If you’re eligible to make a claim, we can act on your behalf on a No Win, No Fee basis so you never pay out of pocket to make a claim.

Do I Pay Tax on a TPD Payout From Super if I’m Under 60?

When your TPD claim is approved, the TPD payout is deposited into your superannuation account, where it forms part of your overall super balance. At this stage, there is no tax payable on your permanent disability benefit (because you haven’t yet accessed the funds).

If you are over 60 years old, you can withdraw your TPD payout tax-free.

If you’re under 60 and choose to withdraw your TPD payout as a lump sum, you will pay tax. While TPD payouts are not classified as taxable income, the withdrawal from your super is subject to superannuation tax rules.

The amount of tax payable will depend on:

Your age at the time of withdrawal

The taxable and tax-free components of your super balance

Your superannuation fund’s policies

It’s important to review your fund’s tax treatment carefully or speak with a TPD lawyer to ensure you understand your entitlements and tax implications before withdrawing your payout.

Do TPD Payouts Affect Centrelink Payments in Australia?

Centrelink is complex and obtaining further advice is highly recommended. In short, approval of a TPD claim will not impact your Centrelink entitlements as it will initially be paid into your superannuation account. However, if you withdraw a TPD lump sum from your superannuation, the withdrawal may affect your Centrelink entitlements, depending on your financial position.

It is important to obtain professional advice prior to withdrawing a lump sum TPD payout to ensure that you are not impacted without knowledge. Our TPD Lawyers can assist you in that regarding, without providing financial advice.

Want more information? Read our blog that covers how TPD can affect your Centrelink payments.

Can You Return to Work After Receiving a TPD Payout from a Superannuation Fund in Australia?

Yes, in many cases you can return to work after receiving a TPD payout from your super fund.

To successfully claim a TPD payout from your superannuation fund, you must demonstrate that you are unable to work in your usual occupation or any role suited to your education, training, or experience (ETE). This is typically supported by a medical statement from your treating doctors certifying that, at the time of the assessment, you were permanently unfit for work.

However, medical practitioners cannot predict the future. If your condition improves over time, and you’re able to retrain or take up a different type of work, you may return to the workforce. Doing so does not automatically cancel your TPD insurance claim or require repayment of the benefit, especially if your eligibility was valid at the time of approval.

It’s essential to understand your super fund’s policy wording and consult a TPD lawyer to clarify your rights if you’re considering returning to work after receiving a superannuation disability payout.

Contact Our No Win No Fee TPD Lawyers Today for a Free Claim Assessment

Our experienced TPD lawyers offer a free claim check to determine whether you have TPD insurance through your superannuation fund and whether you may be eligible to make a TPD claim. We’ll assess your situation before you proceed, with no upfront costs and no obligation.

Contact us today to find out how our No Win No Fee TPD lawyers can help you access the maximum TPD payout you’re entitled to.

Issa Rabaya

• Bachelor of Laws

• Graduate Diploma in Legal Practice

• Approved Legal Service Provider to the Independent Review Office

• Member of the Law Society

Issa Rabaya

• Bachelor of Laws

• Graduate Diploma in Legal Practice

• Approved Legal Service Provider to the Independent Review Office

• Member of the Law Society