To be eligible for a TPD claim, your health condition, illness, or injury must be the reason you can no longer work. Your claim should demonstrate that you are unable to work in any role related to your current education, training, or experience.

However, making a TPD claim does not necessarily prevent you from ever working again. In fact here are 3 possible scenarios we have seen with our clients:

You may start a job in a field you haven’t worked in before, which means you might not have known if you could do it. For example, you could have only been qualified and/or trained to be a carpenter but never worked in sales. Although you may never return to being a carpenter, you decide to try working in sales.

Your health condition, illness, or injury may significantly improve after treatment or a longer period than expected. For example, many clients who were battling cancer and believed they would never return to work have experienced remarkable recoveries and have gone back to their jobs. This positive outcome is incredibly rewarding for us and brings us great joy

Despite making a TPD claim, you might choose to pursue new qualifications or retrain in a field where you previously had no experience or qualifications. This decision allows you to continue moving forward and not give up on your career goals.

Are You Getting What You Are Supposed to From Your TPD claim?

Before looking at what consumers are getting out of their TPD insurance and the effectiveness of their policies, it is important to define Total and

Total & Permanent Disablement (TPD) Superfund in Australia

What is TPD insurance in super? Superannuation, or just super, in short, refers to benefit funds for retirement. Employers are required to make payments to

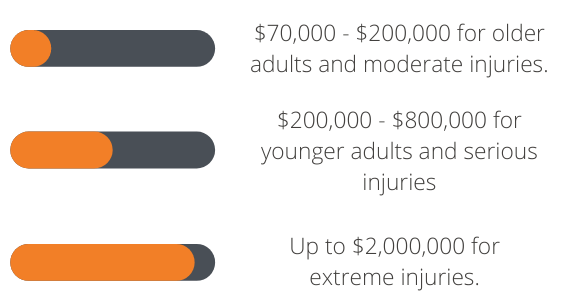

When Should I Settle My Personal Injury Claim?

This is understandably one of the hardest decisions you would need to make in your personal injury claim. Regardless of whether it’s a car accident claim,