TPD vs Income Protection | What's the Difference?

Key takeaway: TPD insurance pays a one-off lump sum, typically between $70,000 and $2,000,000, if you are permanently unable to work in any job suited to your education, training or experience. Income protection instead pays up to 95% of your pre-injury income for the first 6 months, usually reducing to about 70%, while you are temporarily off work.

TPD vs Income Protection: Quick Answers

When you’re unable to work due to illness or injury, understanding the key differences between TPD vs Income Protection insurance is essential for securing your financial future.

While both provide valuable support during challenging times, they serve very different purposes. TPD insurance (Total and Permanent Disability) offers a lump sum payout if you’re permanently unable to return to work, helping cover long-term expenses like mortgages and medical care. In contrast, Income Protection insurance provides regular monthly payments if you’re temporarily unable to work, covering everyday costs until you recover.

Choosing the right option can be complex, which is why speaking with an experienced TPD lawyer or income protection lawyer can make all the difference. In this guide, we explain how each policy works and which may suit your situation best.

TPD vs Income Protection Overview

TPD Insurance (Total and Permanent Disability):

Provides a one-time lump sum payout if you become permanently unable to work in any job suited to your education, training, or experience. It’s designed to help cover long-term expenses, like paying off a mortgage or funding ongoing medical care.

Income Protection Insurance:

Offers a regular income, typically a percentage of your salary, if you’re temporarily unable to work due to illness or injury. This type of insurance is intended to cover everyday expenses until you can return to work or reach the policy’s end date.

What is TPD Insurance?

TPD insurance, or Total and Permanent Disability insurance, is designed to provide a financial safety net if you’re permanently unable to work due to a severe injury or illness. In simple terms, if you can’t return to any job suited to your education, training, or experience because of your condition, TPD insurance can pay out a one-time lump sum.

This payout can be used to cover a range of long-term expenses, such as:

- Paying off your mortgage or other debts

- Funding ongoing medical treatments or rehabilitation

- Modifying your home to accommodate new physical needs

- Supporting your family’s financial well-being

The goal of TPD insurance is to give you and your loved ones some stability and financial security at a time when your income is no longer reliable. This is why most Aussies have TPD cover bundled automatically in their super, even if they don’t know they do.

What is Income Protection Insurance?

Income Protection insurance offers a different kind of financial safety net compared to TPD insurance. Instead of a one-time lump sum, it provides a regular income to someone who is temporarily unable to work due to illness or injury. As a superannuation insurance benefit, Income Protection payments are designed to help cover everyday living expenses while you recover.

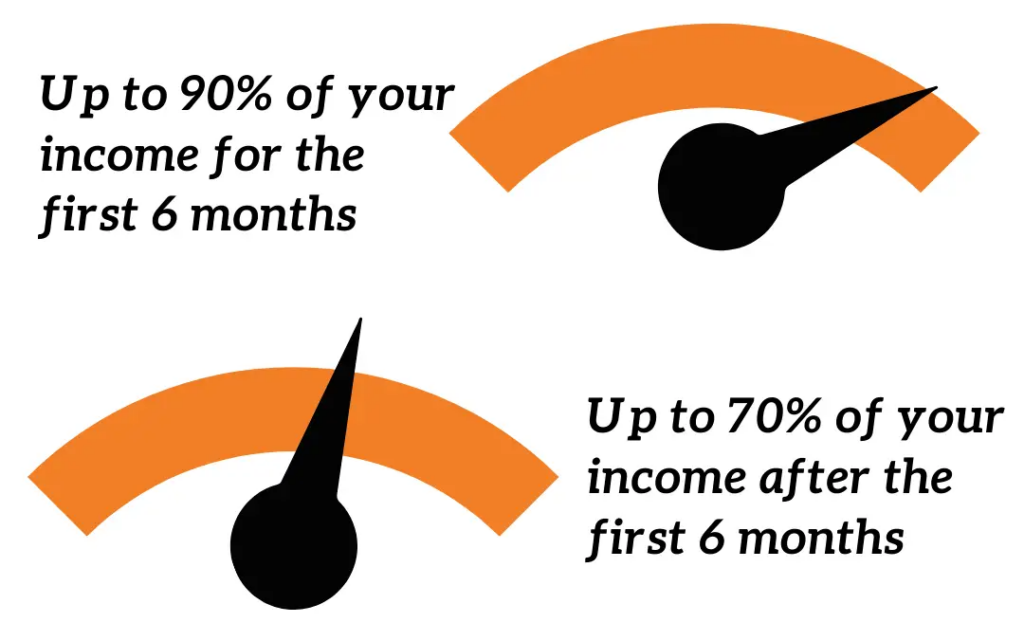

The amount you receive and the duration of the payments depend on the specifics of your policy. Typically, up to 95% of your pre-injury income may be paid during the first six months, with the benefit amount reducing to around 70% after that period.

The length of time you can receive these benefits also varies. Depending on your policy, payments could continue for a set period—such as two or five years—or up until a specified age, like 65. The exact terms are outlined in your superannuation insurance policy, so it’s important to understand your coverage details.

The Key Differences Between TPD vs Income Protection Insurance

| Income Protection | TPD |

|---|---|

| Can be claimed when you are unable to work | Can be claimed if you are no longer able to work in your usual or any occupation based on your education, training and experience |

| Pays a monthly benefit, during a predetermined period | Usually pays a lump sum payment |

| Benefits include up to 95% of the pre-injury income for a period of time of usually 2-5 years | Benefit payouts amount typically range between $70,000 - $2,000,000 |

While not all superannuation funds automatically provide coverage for both, you can opt to have both TPD Insurance and Income Protection to better secure your future. Having both types of coverage can offer greater financial benefits if you become unable to work, providing comprehensive support for your needs.

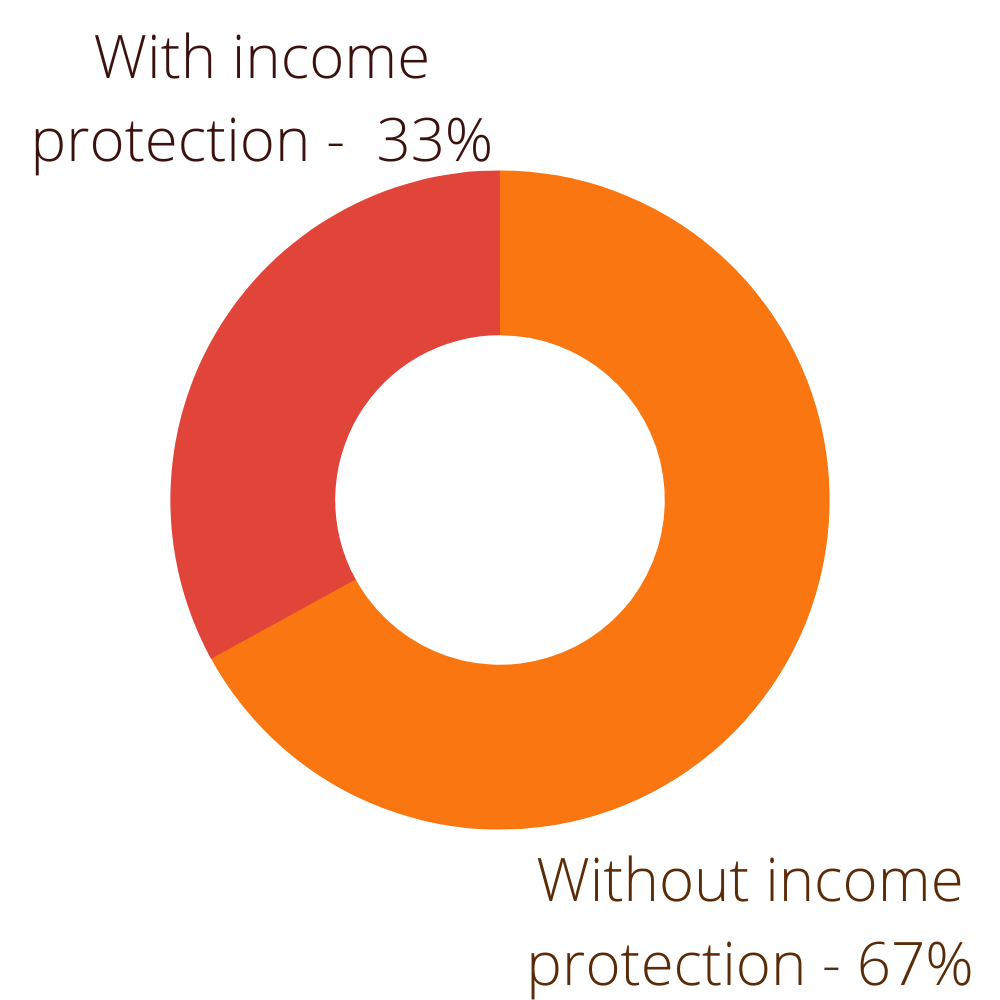

What Percentage of Australians Are Covered by Income Protection Insurance?

According to Rice Warner’s report in 2017, only 33% of Australians have income protection that can financially support them if they become unable to work.

Making a Successful Income Protection Claim in Australia

1. Notify Your Employer and Superannuation Insurer

As soon as you become unable to work, it’s important to reach out to both your employer and your superannuation insurer to initiate your income protection claim. Your insurer will guide you through the process and send you the necessary paperwork to get started.

2. Obtain a Statement from Your GP

Request a detailed statement from your GP confirming that you are unable to work due to your medical condition. This statement will be a crucial piece of evidence to support your claim.

3. Complete the Income Protection Claim Form

Fill out the income protection claim form provided by your superannuation insurance company. Make sure to include all required documents, such as the GP statement, work history, recent payslips, identification, and any other relevant information. If you find the process overwhelming, our TPD lawyers are here to assist you. We often lodge income protection claims alongside TPD claims for our clients, ensuring everything is handled smoothly.

4. Wait for the Outcome

Once you’ve submitted your claim with the correct supporting documentation, your next step is to wait for your insurer’s response. Be aware that most policies have a waiting period of 0 to 90 days before payments can begin.

Can You Have Both TPD and Income Protection Insurance?

Yes, you can hold both types of cover, and for many individuals this is the most comprehensive strategy. Holding both means:

-

You have income protection to keep money flowing if you’re temporarily off work.

-

You have TPD cover to fall back on if you are permanently unable to work.

Important to check: how your policies interact (some super funds may treat them differently), whether there are offsets or definitions that link them, and whether premiums are cost‐effective. TPD and Income Protection lawyers can review your policies, check definitions across both covers, and advise if they are complementary or if one is redundant given your situation.

Injured and unsure if you have the right cover? Contact our TPD and Income Protection Lawyers today for a free claim assessment to find out what you’re eligible to claim.

What Should I Do If My TPD or Income Protection Claim is Refused?

Having your TPD or Income Protection claim refused can be frustrating and overwhelming, especially when you’re already dealing with the stress of being unable to work. But a denied claim doesn’t mean you’re out of options. In many cases, refusals can be challenged successfully with the right guidance.

The first step is to carefully read the insurer’s denial letter to understand their reasons for rejecting your claim. This might include issues like insufficient medical evidence, policy exclusions, waiting period disputes, or a narrow interpretation of your disability. From there, gathering stronger medical evidence, clarifying factual errors, or challenging unfair interpretations can significantly improve your chances.

At Withstand Lawyers, we specialise in helping Australians overturn denied TPD and Income Protection claims. Our lawyers can review your policy, assess the denial, identify weaknesses in the insurer’s reasoning, and guide you through the appeal or dispute process. We handle communication with the insurer on your behalf, gather supporting evidence, and ensure your rights are protected at every step.

If your claim has been refused, don’t navigate it alone. Contact us today for a free claim assessment and get clear advice on your best next steps.

When to Speak to a TPD or Income Protection Lawyer

You should speak with a TPD or Income Protection Lawyer when:

-

You’re about to lodge a claim and your policy wording is unclear (definitions like “own occupation”, “any occupation”, “unable to return to work”).

-

You’ve had a claim rejected or delayed and you suspect the insurer misinterpreted your policy.

-

You’re unsure whether your condition meets the “total & permanent” threshold for TPD or the “unable to work” threshold for Income Protection.

-

You’re self‑employed, contractor, or have complex income structures (which complicate income protection claims).

A qualified TPD lawyer or income protection lawyer will review the Product Disclosure Statement (PDS), claim history, insurer communications and your medical evidence. Engaging legal support early often improves your claim outcome and may reduce stress and errors.

Contact our TPD and Income Protection Lawyers today for a free claim assessment to see where you stand after an injury. We can act on your behalf on a No Win No Fee basis to ensure you get the maximum compensation available.

Success Stories: Real Example of a Successful Income Protection Claim

The Case

Liam, a 48-year-old dad juggling the responsibilities of raising three kids, had built a stable life for his family through his work as a bookkeeper, earning $90,000 a year. But in 2020, a sudden and serious back injury struck while he was at home, leaving him in pain and unable to work. To make matters worse, the nature of the injury at home mean that Liam wasn’t eligible for any personal injury claim. The situation left him facing both physical challenges and financial uncertainty.

The Outcome

Thankfully, Liam had income protection insurance, which became his financial lifeline while he was stuck at home and unable to work. The insurance provided him with monthly payments to cover his daily expenses and support his family. During the first six months, he received $6,180 each month—90% of his pre-injury salary. After the sixth month, the payments adjusted to $5,150, equaling 75% of his previous income.

When he finally recovered and was ready to get back to work, the income protection payments stopped. But during those challenging months, the financial support made all the difference, allowing him to focus on healing without the constant worry of bills piling up.

TPD was not a factor in Liam’s case as he was able to return to work in his field.

To read about injuries that lead to TPD claims, click here.

Reach our Superannuation Lawyers for a Free Claim Check

Our experienced superannuation lawyers specialise in TPD and income protection claims and offer a free claim check to assess your case if you are injured or unable to work. We work on a No Win, No Fee basis, meaning you’ll only be charged if we successfully win your case, and you won’t pay any upfront costs.

Our TPD lawyers are ready to help. Whether you’re just starting your superannuation claim or facing hurdles along the way, we’re here to ensure you receive your full entitlements as quickly as possible.

Reach out to us anytime at 1800 952 898 or fill out our online form for a free claim assessment today.

TPD vs Income Protection FAQs

What is the difference between TPD and income protection?

Can you have both TPD and income protection insurance?

How long does income protection pay for?

How much does TPD pay compared to income protection?

Can I claim TPD and income protection at the same time?

What percentage of Australians have income protection insurance?

How do I make a successful income protection claim?

What should I do if my TPD or income protection claim is refused?

About the author

Issa Rabaya · Principal Lawyer and Director

✓ Admitted to the Supreme Court of NSW and High Court of Australia ✓ LLB ✓ IRO-approved ✓ Law Society of NSW

Acts for injured people in CTP, workers compensation, TPD and public liability claims.

Why Choose Withstand Lawyers for Your TPD or Income Protection Claim?

When illness or a serious injury stops you working, choosing between policies and definitions is the last thing you need. Withstand Lawyers reviews your superannuation cover, tells you plainly what you can claim, and runs your TPD or income protection claim from lodgement to payout. Withstand Lawyers brings decades of experience, more than $47 million recovered for clients and a 99% success rate to every claim, including refused and delayed ones. With Withstand Lawyers there are never upfront costs, because every claim is handled on a No Win No Fee basis.

Call 1800 952 898 for a free claim check. No win, no fee, no upfront costs.

★ 4.9 on Google (265+ reviews)